Indian Real Estate Set to Soar, Targeting a $1 Trillion Milestone by 2030

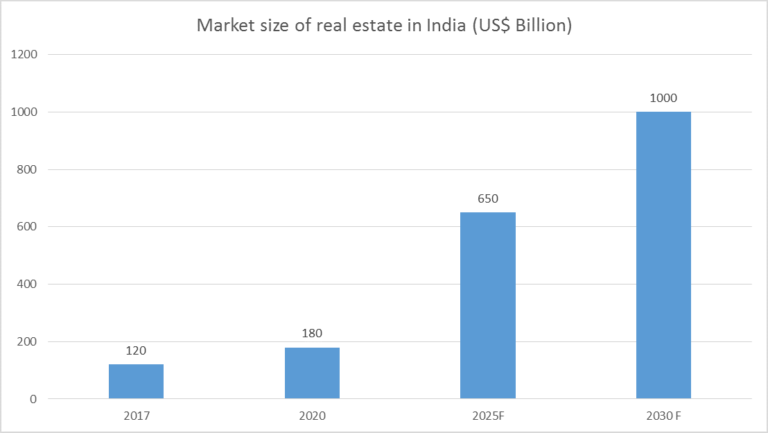

The Indian real estate industry is projected to achieve a market size of US$ 1 trillion by 2030, constituting approximately 18-20% of India’s GDP.

ADVANTAGES IN INDIA

ROBUST DEMAND

- Savills India predicts a 15-18 million sq. ft. surge in data center demand in the coming years.

- Luxury residential market sales experienced an impressive 151% year-over-year (y-o-y) growth during the first quarter of 2023.

- It is anticipated that organized retail real estate stock will grow by 28% to reach 82 million sq. ft. by 2023.

ATTRACTIVE OPPORTUNITIES

- According to ICRA estimates, Indian companies are anticipated to raise over Rs. 3.5 trillion (equivalent to US$ 48 billion) in 2022, contrasting with the previously accumulated funds totaling US $29 billion.

- Additionally, the prominent private market investor, Blackstone, known for its substantial investments in the Indian real estate sector valued at Rs. 3.8 lakh crore (US$ 50 billion), is actively pursuing further investments amounting to Rs. 1.7 lakh crore (US$ 22 billion) by 2030.

POLICY SUPPORT

- Fueled by growing transparency and improved returns, there is a notable upswing in private investments within the sector.

- Additionally, the government has granted permission for up to 100% foreign direct investment (FDI) in township and settlement development projects.

- Furthermore, the Union Budget for 2023-24 has unveiled a commitment of Rs. 79,000 crore (equivalent to US$ 9.64 billion) for the PM Awas Yojana, signifying a 66% increase in comparison to the previous year

INCREASING INVESTMENT

- The Private Equity Investments in India’s real estate sector, stood at US$ 4.2 billion in 2023.

- FDI in the sector (including construction development & activities) stood at US$ 55.5 billion from April 2000-December 2022.

INTRODUCTION

The real estate sector holds international recognition as one of the key industries, encompassing four primary sub-sectors: housing, retail, hospitality, and commercial. Its expansion harmonizes with the growth of the corporate landscape, the need for office spaces, and the rising demand for urban and semi-urban housing. Notably, the construction industry stands as the third-largest among the 14 major sectors, influencing the economy through its direct, indirect, and induced effects.

Within India, the real estate sector serves as the second-largest employment generator, surpassed only by the agriculture sector. Furthermore, it is anticipated that the sector will witness an increased influx of investments from non-resident Indians (NRIs), both in the immediate and extended periods. Bengaluru is poised to emerge as the foremost choice for NRI property investments, followed by Ahmedabad, Pune, Chennai, Goa, Delhi, and Dehradun in the hierarchy of favored investment destinations.

MARKET SIZE

By the year 2040, the real estate market is projected to expand to Rs. 65,000 crore (equivalent to US$ 9.30 billion), a significant leap from the Rs. 12,000 crore (US$ 1.72 billion) recorded in 2019. The Indian real estate sector is on a promising trajectory, with expectations of reaching a remarkable US$ 1 trillion in market size by 2030, up from US$ 200 billion in 2021, and contributing a substantial 13% to the nation’s GDP by 2025. The growth extends to retail, hospitality, and commercial real estate, which are all playing pivotal roles in meeting India’s burgeoning infrastructure demands.

In the fiscal year 2023, the residential property market in India achieved remarkable milestones. Home sales soared to an all-time high, valued at Rs. 3.47 lakh crore (equivalent to US$ 42 billion), reflecting an impressive year-on-year growth of 48%. In terms of volume, the sector experienced a robust surge, with a 36% increase and a total of 379,095 units sold.

Indian real estate developers operating in the country’s major urban centers are poised for a remarkable achievement in 2023, as they are on track to complete approximately 558,000 homes.

In the first nine months of the fiscal year 2022, India’s real estate sector witnessed land deals covering more than 1,700 acres in the top eight cities. Over the span of 2017-2021, foreign investments in the commercial real estate sector reached a substantial figure of US$ 10.3 billion. As of February 2022, developers are anticipating a surge in demand for office spaces within Special Economic Zones (SEZs) following the replacement of the existing SEZs act.

According to ICRA estimates, Indian companies are projected to raise over Rs. 3.5 trillion (equivalent to US$ 48 billion) through infrastructure and real estate investment trusts in 2022, marking significant growth from the funds raised up to the present, totaling US$ 29 billion.

In the top eight cities, the office market witnessed transactions totaling 22.2 million square feet from July 2020 to December 2020, while new completions amounted to 17.2 million square feet during the same period. Sector-wise occupancy shares were as follows: the Information Technology (IT/ITeS) sector led with a 41% share in the latter half of 2020, followed by the BSFI and Manufacturing sectors, each with 16%, while Other Services and Co-working sectors contributed 17% and 10%, respectively.

In 2021, approximately 40 million square feet of real estate was delivered in India. It is projected that India will capture a 40% market share over the next 2-3 years, with expectations of delivering 46 million square feet in 2022.

According to Savills India, there is a growing demand for data centers in the real estate sector, and it is anticipated that this demand will increase by 15-18 million square feet by 2025.

In the year 2020, the manufacturing sector secured a notable share, leasing 5.7 million square feet of office space, which accounted for 24% of the total. Among the key leasing sectors, SMEs and electronic component manufacturers dominated, with strong activity in Pune, Chennai, and Delhi NCR. Additionally, the auto sector played a significant role in leasing, primarily in Chennai, Ahmedabad, and Pune. The office space leasing was diversified, with 3PL (Third-Party Logistics), e-commerce, and retail segments contributing 34%, 26%, and 9% of the total office space leases, respectively.

Moreover, in the final quarter of the fiscal year 2021, among the total private equity (PE) investments in real estate, the office segment attracted the largest share, accounting for 71%, while retail secured 15%, and residential and warehousing held 7% each of the investments.

In 2022, the absorption of office space in the top seven cities amounted to 38.25 million square feet.

During the first quarter of 2023 (January-March), the net office space absorption in the top six cities reached 8.3 million square feet.

In the same quarter of 2023, fresh real estate launches in India’s top seven cities accounted for 41% of the total market share, a notable increase from the 26% recorded four years earlier. Out of the approximately 1.14 lakh units sold across these cities in the first quarter of 2023, over 41% constituted newly launched properties.

Between July 2021 and September 2021, the third quarter of 2021 witnessed a substantial surge in new housing supply, with approximately 65,211 units launched across the top eight cities, marking a remarkable 228% year-on-year increase compared to the approximately 19,865 units launched in the third quarter of 2020.

In the fiscal year 2021-22, the commercial real estate sector is expected to witness a surge in investments. For example, in October 2021, Chintels Group disclosed plans to invest Rs. 400 crore (equivalent to US$ 53.47 million) in the development of a new commercial project spanning 9.28 lakh square feet in Gurugram. Notably, the transactions in the commercial real estate sector experienced significant growth, doubling to reach 1.5 million square feet in the first quarter of 2023.

As highlighted during the Economic Times Housing Finance Summit, the current construction rate stands at approximately three houses built per 1,000 people annually, falling short of the required rate of five houses per 1,000 population. This disparity has resulted in an estimated housing shortage of around 10 million units in urban areas. To accommodate the nation’s urban population growth, an additional 25 million units of affordable housing are projected to be needed by the year 2030.

INVESTMENTS/DEVELOPMENTS

The Indian real estate sector has experienced substantial growth recently, driven by increasing demand for both office and residential spaces.

Private equity investments in India’s real estate sector reached US$ 4.2 billion in 2023, reflecting a positive trend.

In 2022, private equity investments in India’s real estate sector amounted to US$ 3.4 billion, underscoring the sector’s attractiveness to investors.

Notably, India’s real estate sector has witnessed a remarkable three-fold increase in foreign institutional inflows, with an impressive total of US$ 26.6 billion recorded during the period spanning 2017-2022.

Exports from Special Economic Zones (SEZs) have shown substantial growth, reaching Rs. 7.96 lakh crore (equivalent to US$ 113.0 billion) in FY20, marking a 13.6% increase from the previous year when it was Rs. 7.1 lakh crore (US$ 100.3 billion) in FY19.

In a move to enhance accessibility for small and retail investors, in July 2021, the Securities and Exchange Board of India (SEBI) reduced the minimum application value for Real Estate Investment Trusts (REITs) from Rs. 50,000 (US$ 685.28) to Rs. 10,000-15,000 (US$ 137.06 – US$ 205.59).

Foreign Direct Investment (FDI) in the sector, which includes construction development and related activities, amounted to US$ 55.5 billion from April 2000 to December 2022.

Here are some of the significant investments and developments within this dynamic sector:

- During the fiscal year 2023, Delhi-NCR secured a substantial 32% share of the total private equity (PE) investments in the real estate sector.

- In the first quarter of 2023, there was a remarkable 151% year-over-year (y-o-y) growth in luxury residential market sales, spanning from January to March.

- Housing sales in India’s top seven cities reached 1.14 lakh units during the first quarter of 2023, reflecting a notable increase of over 99,500 units in comparison to the same period in 2022.

- In the first quarter of 2023, Bengaluru, Delhi-NCR, and Chennai jointly contributed to two-thirds of the quarterly demand. Flexible workspace, at 27%, emerged as the most significant contributor to this demand.

- As of June 5, 2023, a total of 119.7 lakh houses have received sanctions under the Pradhan Mantri Awas Yojana-Urban (PMAY-U), with 74.75 lakh houses successfully completed and delivered to urban individuals in need.

- Between January and July 2022, the real estate sector in India witnessed private equity investment inflows amounting to US$ 3.27 billion, indicating a positive trend.

- In 2022, home sales across India’s top eight cities exhibited a remarkable 68% year-on-year (YoY) increase, with approximately 308,940 units sold, signaling a robust recovery in the real estate sector.

- The retail real estate segment attracted institutional investments totaling US$ 492 million in 2022, highlighting the sector’s appeal to investors.

- During the third quarter of 2021, institutional real estate investment in India experienced a notable 7% YoY growth. The total investments in the first nine months of 2021 reached US$ 2,977 million, compared to US$ 1,534 million during the same period in the previous year.

- In November 2021, Ascendas India secured a significant deal by acquiring a 16-storey commercial tower in Navi Mumbai from Aurum Ventures for Rs. 353 crore (equivalent to US$ 47 million). This transaction marked one of the most substantial standalone commercial tower deals executed by a global institutional investor in recent years.

- In 2021, Housing.com, an online real estate company owned by REA India, collaborated with online legal assistance start-ups including LegalKart, Lawrato, Vidhikarya, and Vakil to provide legal advice and support to homebuyers.

- The top three cities, namely Mumbai (comprising around 39%), NCR-Delhi (about 19%), and Bengaluru (also around 19%), collectively attracted approximately 77% of the total investments recorded in the third quarter of 2021.

- A report by CBRE suggests that India’s flexible office space stock is poised to expand by 10-15% year-on-year, surpassing the current 36 million square feet, within the next three years.

- In June 2021, GIC announced its intention to acquire a minority stake in Phoenix Mills’ portfolio valued at US$ 733 million, with the goal of establishing an investment platform for Indian retail-led mixed-use assets.

- Blackstone Real Estate made a significant acquisition in May 2021, acquiring Embassy Industrial Parks for Rs. 5,250 crore (equivalent to US$ 716.49 million) to enhance its presence in India.

- The SRAM & MRAM Group entered the Indian real estate market through collaboration with Area CAS Developers and Infrastructure Private Limited (Area Group) and Gupta Builders and Promoters Private Limited (GBP Group) in a move involving an investment of US$ 100 million.

- Anarock’s data revealed that housing sales in seven cities surged by 29%, while new launches increased by 51% in the fourth quarter of fiscal year 2021 compared to the same period in the previous year.

- Private market investor Blackstone, with substantial investments in the Indian real estate sector worth Rs. 3.8 lakh crore (US$ 50 billion), has expressed its intent to invest an additional Rs. 1.7 lakh crore (US$ 22 billion) by the year 2030.

- In 2021, the swift adoption of remote working has fueled the demand for affordable housing units with a ticket size below Rs. 40-50 lakh, and this surge is anticipated to drive price increases in Tier 2 and 3 cities across India.

- In April 2021, HDFC Capital Advisors (HDFC Capital) joined forces with Cerberus Capital Management (Cerberus) to establish a platform dedicated to identifying high-yield opportunities within the Indian residential real estate sector. This platform aims to acquire housing inventory and offer last-mile funding for ongoing residential projects nationwide.

- Godrej Properties made significant moves in March 2021, with the announcement of the launch of 10 new real estate projects in the fourth quarter.

- In the same month, Godrej Properties further solidified its presence in the real estate sector by increasing its equity stake in Godrej Realty from 51% to 100%, achieved through the acquisition of equity shares from HDFC Venture Trustee Company.

- In January 2021, SOBHA Limited’s wholly owned subsidiary, Sabha Highrise Ventures Pvt. Ltd., completed the acquisition of a 100% share in Annalakshmi Land Developers Pvt. Ltd.

GOVERNMENT INITIATIVES

The Government of India, in collaboration with the state governments, has undertaken numerous initiatives to promote growth within the real estate sector. Notably, the Smart City Project, aimed at constructing 100 smart cities, presents a significant opportunity for real estate companies. Additionally, there are several other prominent government initiatives in this regard:

- In the Union Budget for 2023-24, the Finance Ministry unveiled a commitment of Rs. 79,000 crore (equivalent to US$ 9.64 billion) for the PM Awas Yojana, marking a significant 66% increase compared to the previous year.

- In October 2021, the Reserve Bank of India (RBI) decided to maintain the benchmark interest rate at 4%, providing a substantial boost to the real estate sector in India. The regime of low home loan interest rates was expected to drive housing demand, leading to a projected sales increase of 35-40% during the festive season in 2021.

- The Union Budget for 2021-22 extended tax deductions for interest on housing loans and tax holidays for affordable housing projects until the end of the fiscal year 2021-22.

- As part of the Atmanirbhar Bharat 3.0 package, announced by Finance Minister Mrs. Nirmala Sitharaman in November 2020, income tax relief measures were introduced for real estate developers and homebuyers, specifically for primary purchase/sale of residential units with a value of up to Rs. 2 crore (equivalent to US$ 271,450.60) from November 12, 2020, to June 30, 2021.

- To address the revitalization of approximately 1,600 stalled housing projects in prominent cities across the nation, the Union Cabinet has granted approval for the establishment of a Rs. 25,000 crore (equivalent to US$ 3.58 billion) alternative investment fund (AIF).

- The Government has established an Affordable Housing Fund (AHF) within the National Housing Bank (NHB), commencing with an initial corpus of Rs. 10,000 crore (US$ 1.43 billion). This fund utilizes the priority sector lending shortfall of banks and financial institutions to facilitate micro-financing for Housing Finance Companies (HFCs).

- By December 31, 2022, India had formally approved 425 Special Economic Zones (SEZs), and as of January 2023, 270 SEZs have become operational. It’s worth noting that the majority of these SEZs are focused on the Information Technology (IT) and Business Process Management (BPM) sectors.

ROAD AHEAD

The Securities and Exchange Board of India (SEBI) has granted approval for the Real Estate Investment Trust (REIT) platform, opening up opportunities for various types of investors to participate in the Indian real estate market. This move is expected to create a significant opportunity worth Rs. 1.25 trillion (equivalent to US$ 19.65 billion) in the Indian market in the coming years.

Responding to an increasingly informed consumer base and considering the impact of globalization, Indian real estate developers have embraced new challenges. Notably, there has been a noticeable transition from family-owned businesses to professionally managed ones.

To efficiently manage multiple projects across different cities, real estate developers are investing in centralized processes for material sourcing and workforce organization. They are also hiring qualified professionals in fields such as project management, architecture, and engineering.

The residential sector is anticipated to experience substantial growth, with the central government aiming to construct 20 million affordable houses in urban areas throughout the country by 2022 under the ambitious Pradhan Mantri Awas Yojana (PMAY) scheme of the Union Ministry of Housing and Urban Affairs. This growth in the number of housing units in urban areas is expected to drive demand for commercial and retail office spaces.

It’s important to note that there is a current shortage of approximately 10 million housing units in urban areas. To accommodate the urban population’s growth, an additional 25 million units of affordable housing are projected to be needed by 2030.

The increasing influx of Foreign Direct Investment (FDI) into the Indian real estate sector is fostering greater transparency. Developers, in their pursuit of funding, have overhauled their accounting and management systems to meet due diligence standards. India’s real estate market is poised to attract a significant amount of FDI in the next two years, with an expected capital infusion of US$ 8 billion by fiscal year 2022