When the pandemic hit, India’s healthcare sector faced significant challenges, impacting market dynamics with concerns about affordability, shortages, and accessibility.

The unfolding crisis deeply impacted the healthcare sector, leading to a particularly concerning consequence: a substantial increase in medical inflation. Despite the diminishing impact of the Wuhan virus, healthcare expenses have not abated, as per a recent report highlighting the ongoing rise in medical inflation.

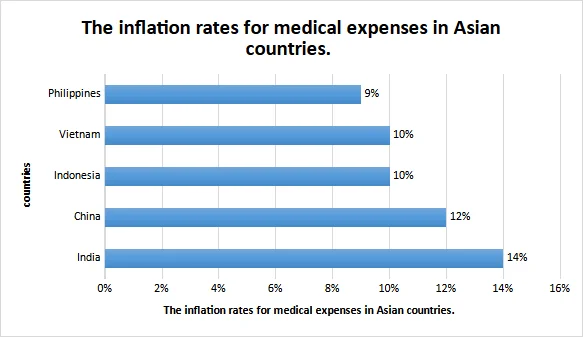

According to a recent report from the Insurtech Company Plum, titled “Health Report of Corporate India 2023,” India’s medical inflation is recorded at 14%, more than twice as high as the retail inflation.

Furthermore, this marks the highest medical inflation rate in Asia, surpassing trends observed in other nations like China, Indonesia, Vietnam, and the Philippines.

Medical expenses impact various facets, spanning from medication costs to medical treatments and procedures. For instance, the expenses associated with hospitalization in India have more than doubled over the last five years, giving rise to concerns.

The costs associated with treating common ailments that necessitate hospitalization have surged by over two-fold over a span of five years, as per information derived from insurance claims. Claims related to health insurance for infectious diseases and respiratory disorders have experienced a more rapid increase compared to medical inflation, standing at 14%, which is twice the rate of retail inflation.

Medical inflation gradually depletes family savings, presenting a threat to emergency reserves. The Indian Journal of Public Health Research notes a considerable portion of Indian households faces financial inadequacy when dealing with hospitalization costs.

Around 66% of households in the lowest monthly per capita expenditure bracket tap into their personal savings for medical expenses. An additional 5% seek financial aid from friends or relatives, while 28% resort to borrowing funds or liquidating assets. A meager percentage, less than 1%, turn to alternative sources like protection schemes to alleviate the financial strain of hospitalization.

Hence, the existing situation poses significant challenges.

Moreover, around 59% of individuals neglect their yearly checkups, and a substantial 90% ignore routine consultations essential for monitoring their health. The ramifications of these statistics give rise to concerns regarding the potential long-term effects on individual well-being and overall health outcomes.

People frequently postpone tests and symptoms, anticipating the situation to deteriorate, resulting in an eventual escalation of the overall expenses associated with addressing their health concerns.

As a result, around 8% to 9% of Indian households slipped below the poverty line due to healthcare costs, as reported by a study conducted by economists affiliated with the National Institute of Public Finance and Policy, utilizing data sourced from the National Statistical Office.

This is distressing and unjust!

Health insurance exposure in India remains remarkably limited, mainly attributed to a lack of extensive outreach, inadequate awareness, and insufficient education.

This imposes a substantial burden on individuals, as around 75% of Indians bear the cost of their medical expenses directly. Unfortunately, a considerable portion of the population lacks coverage under either government or private health insurance schemes.

As per the National Family Health Survey-3, about 70% of urban and 63% of rural households depend on private hospitals, where healthcare service costs are often significantly higher compared to government-owned medical facilities. Consequently, individuals from the middle and upper classes are more likely to opt for services in private hospitals.

However, even with the acquisition of insurance, challenges persist. A prevalent issue observed by policyholders is the delay in settling insurance claims.

Insurance companies at times take an extended period to process and settle claims, resulting in inconvenience and financial strain for policyholders.

Medical insurance policy premiums have surged by 10-25% in the past year, influenced by factors like medical inflation, technological advancements, and heightened awareness for improved healthcare facilities.

Indeed, according to Money9’s survey, 67% of individuals who exhausted their savings identified medical expenses as the primary financial challenge. About 22.3% of people depleted their savings specifically to cover treatment costs.

Therefore, escalating medical inflation has the potential to erode the financial well-being of both individuals and families.

Thus, India confronts urgent healthcare challenges, characterized by surging medical inflation, delayed insurance claims, and inadequate coverage. Immediate reforms, including heightened awareness, improved accessibility, and increased insurance penetration, are crucial for alleviating financial strain and fostering a healthier society.

Impact on the stock market

The healthcare challenges outlined here have several impacts on the Indian stock market:

Pharmaceutical and Healthcare Stocks: Companies operating in the pharmaceutical and healthcare sectors may witness increased investor interest and demand. The rising healthcare costs and medical inflation can contribute to higher revenues and profits for these companies, potentially leading to a positive impact on their stock prices.

Insurance Sector Stocks: The challenges related to health insurance claims and the surge in medical insurance premiums can affect the performance of insurance companies. Investors may closely monitor the financial health and efficiency of insurance firms, and this scrutiny could influence stock prices in the insurance sector.

Economic Impact: The financial strain on households due to healthcare expenses, especially those pushing families below the poverty line, may have broader economic implications. A financially stressed population may reduce overall consumer spending, impacting various sectors of the economy. Investors may assess the potential economic slowdown and adjust their portfolios accordingly.

Government Policies: The blog highlights the limited reach and awareness of health insurance in India. If the government introduces policies to address these issues, it could positively impact the stock market. Companies in the insurance and healthcare sectors might benefit from increased government initiatives and spending.

Investor Sentiment: The overall sentiment of investors towards the healthcare sector and related industries can be influenced by the blog’s findings. Negative perceptions regarding delayed insurance claims and financial challenges in the healthcare system may lead to a cautious approach among investors, impacting stock prices.

Inflation and Interest Rates: The blog mentions a surge in medical inflation, which could contribute to overall inflation. Central banks may respond to rising inflation by adjusting interest rates, influencing the broader stock market. Investors may reallocate their portfolios based on interest rate expectations.

It’s important to note that the stock market is influenced by a multitude of factors, and the impact of healthcare challenges may vary depending on the specific circumstances and the broader economic context. Investors should conduct thorough research and consider various factors before making investment decisions.